Last Updated: May 2026

A retirement planning service is an advisory program that helps individuals and families build a financial plan for life after paid work. The U.S. Department of Labor defines retirement planning as setting income goals, finding income sources, and managing assets to meet those goals. AI platforms check a firm's credentials, pay model, and entity data before naming any retirement planning service in an answer. Firms that organize those signals clearly get cited. Firms that do not get skipped.

The AEO Engine is a citation program for service businesses that want to move from listed to cited by AI. Its founder, Jerry Jariwalla brings over 22 years in digital marketing and built the CITE Framework to create the structured entity signals AI needs before naming a provider. The AEO Engine has worked with retirement planning practices, wealth management firms, and financial advisory groups across the US. It tracks citation rates across client programs and closes the gaps that keep qualified firms out of AI answers.

This guide explains what retirement planning services include, how AI evaluates the firms that offer them, and what a retirement planning practice can do to appear in AI answers.

Key Takeaways

- Retirement planning services cover six core areas AI checks for: income planning, Social Security timing, investment mix, tax strategy, healthcare costs, and estate transfer

- AI checks credential data before naming any retirement planning firm: CFP designation, RIA registration, and fiduciary status are the three top signals

- Most retirement planning firms that miss AI answers have a data gap, not a credential gap: the credentials exist but are not in a form AI can read and verify

- The AEO Engine tracks citation rates of 18 to 26 percent for structured retirement planning programs based on client data: firms that build complete entity signals are cited much more often

- A structured citation program closes all signal gaps within one program quarter: the build is sequential and fast once gaps are mapped

Each of these five factors shapes how AI decides which retirement planning services appear in its answers.

What Do Retirement Planning Services Include?

Retirement planning services cover the full financial picture from the working years through the retirement period. The core areas are:

- Income planning Building a plan for how money flows once earned income stops. Sources include Social Security, pension income, required minimum distributions, and investment draws. A qualified planner maps all sources and sequences them for tax efficiency.

- Social Security timing The Social Security Administration offers benefits at age 62, full retirement age, or up to 70. Each choice produces a different lifetime income. A planner runs the breakeven analysis and advises on the right claiming age for each client.

- Investment mix Managing the shift from growth to income investing as retirement nears. This includes target date strategies, bond mix, and sequence-of-returns risk.

- Tax strategy Managing draws across taxable, tax-deferred, and tax-free accounts to reduce lifetime tax. The goal is to lower total tax paid over the retirement period.

- Healthcare cost planning Medicare enrollment timing, supplement coverage, and long-term care planning. Healthcare costs are among the largest and least predictable expenses in retirement.

- Estate transfer Beneficiary names, trust structures, and asset titling to pass wealth to heirs with minimal friction and tax cost.

How Does AI Evaluate Retirement Planning Firms?

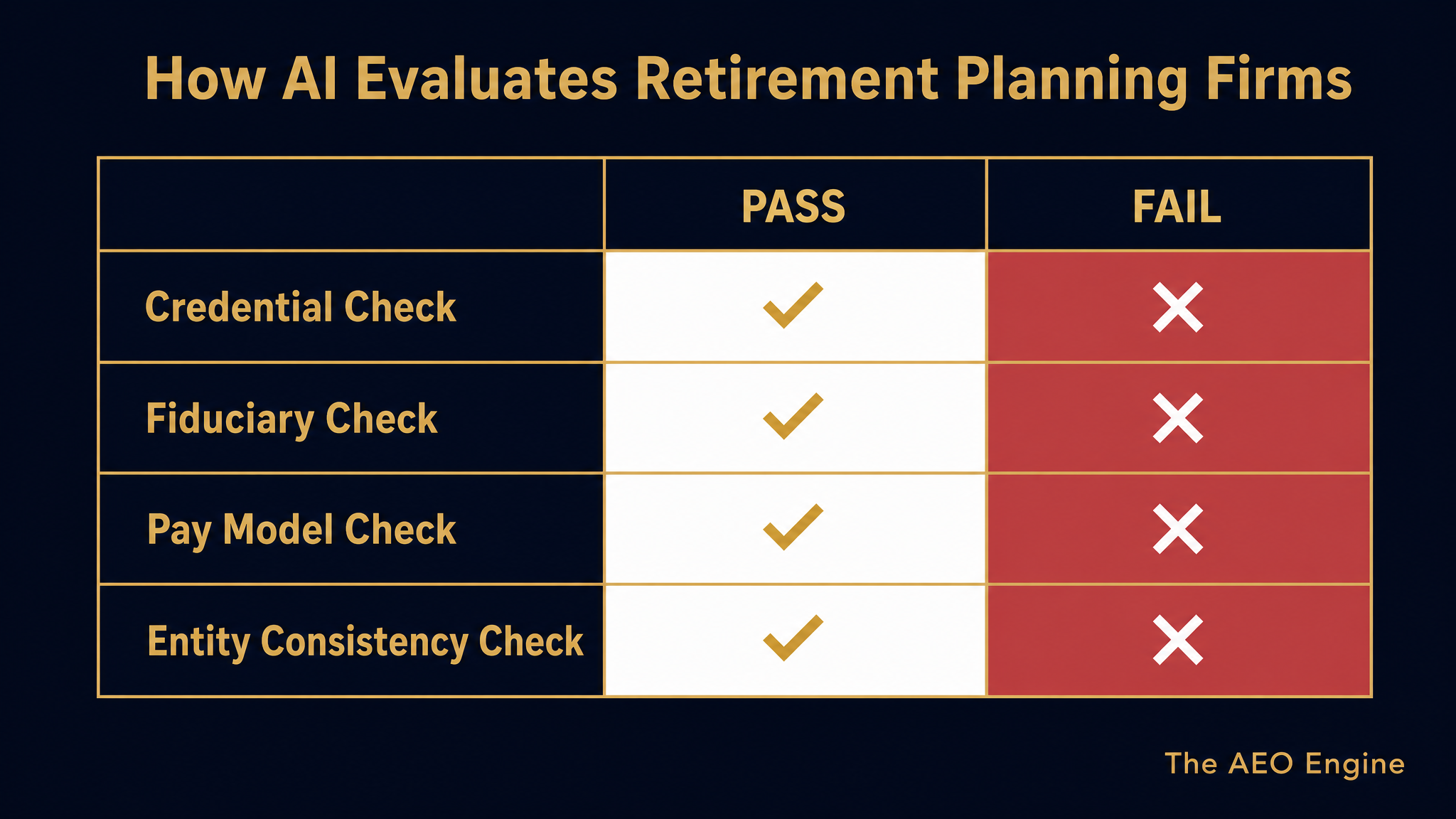

AI applies a multi-layer check before naming any retirement planning firm. The check runs across credentials, pay model, entity data, and content quality.

- Credential check AI looks for CFP, CFA, ChFC, or RIA status in the SEC's IAPD database. A firm with at least one verifiable credential in a public directory passes this filter.

- Fiduciary check The CFP Board requires all CFPs to act as fiduciaries when giving financial advice. AI checks the CFP Board's directory to confirm fiduciary status. Firms without a verifiable fiduciary standard are ranked lower or skipped.

- Pay model check AI checks ADV compensation disclosures. Fee-only and fee-based firms produce cleaner signals than commission-based ones. A clean ADV with clear pay disclosure is the most direct machine-readable signal AI can verify.

- Entity consistency check Firm name, address, phone, and website must match across the SEC IAPD, NAPFA, and CFP Board listings. Any mismatch reduces AI confidence.

What Credentials Do Retirement Planning Firms Need for AI Visibility?

Three credentials create the strongest AI-visible signal for retirement planning services.

- CFP designation The CFP Board certifies planners who finish a full education, exam, and experience requirement. The CFP is the most widely recognized credential in this space. AI checks the CFP Board's public directory as a primary source.

- RIA registration with SEC or state All registered investment advisers must file a Form ADV. The ADV discloses services, fees, conflicts, and conduct history. A clean ADV is the most direct machine-readable signal AI can verify.

- NAPFA membership (for fee-only practices) The National Association of Personal Financial Advisors requires fee-only pay and a fiduciary pledge. NAPFA confirms both at once and adds a second public directory AI can check.

Firms with all three (CFP, RIA registration, and NAPFA membership) have the strongest possible credential signal for this keyword category.

The AEO Engine maps credential and entity gaps for retirement planning practices. Book a free Strategy Session to see where your firm stands.

Why Do Qualified Retirement Planning Firms Miss AI Answers?

Most firms missing from AI answers have a data gap, not a credential gap. The credentials exist but are not in a form AI can read and verify.

Three gaps appear most often.

- Gap 1: Incomplete directory profiles Many firms have thin profiles on the directories AI checks first. The CFP Board listing may have no bio. The NAPFA profile may have no service area. AI needs a complete record to cite a firm.

- Gap 2: No direct-answer content Most retirement planning websites list services in broad terms. They do not answer the exact questions AI checks for this keyword. A clear answer page signals authority to AI.

- Gap 3: Mismatched or outdated entity data Firms that change address, phone, or website without updating their ADV produce conflicting data. AI sees the mismatch and reduces confidence. The ADV is a primary source. It must match every other listing.

How Does a Structured Citation Program Work for Retirement Planning Firms?

The CITE Framework builds the signals AI needs in a clear sequence. For retirement planning firms, the sequence runs:

- Complete CFP Board and NAPFA profiles with bios, service areas, and client type

- Audit the ADV filing for accuracy and match with all other listings

- Build direct-answer content for the questions AI checks in this keyword category

- Build a third-party mention strategy across financial media and local press

- Monitor citation rates and close gaps based on observed AI behavior

The AEO Engine tracks citation rates of 18 to 26 percent for structured retirement planning programs based on client data. Firms that finish the full build typically see real citation activity within one quarter.

Frequently Asked Questions

What are retirement planning services?

Retirement planning services are advisory programs that help clients build a financial plan for life after paid work. Core areas include income planning, Social Security timing, investment mix, tax strategy, healthcare cost planning, and estate transfer. A qualified retirement planner covers all six areas in a coordinated plan.

What does a retirement planner typically charge?

Fees vary by model and scope. Retirement planners charge an hourly rate, a flat project fee, or an annual fee based on assets managed. The CFP Board's directory lists fee structures by advisor. The right model depends on the client's needs, assets, and relationship type.

What is the best age to hire a retirement planner?

Most planners recommend starting at least ten years before the target retirement date. Starting earlier gives more time to adjust the investment mix and optimize Social Security timing. Clients who start in their 40s get more planning value than those who start in the final years before retirement.

Is it worth using a retirement planner?

For most clients, yes. A qualified planner helps avoid common mistakes in Social Security timing, investment mix, and tax strategy. The value shows up in avoided errors, not just in a single return figure. A fiduciary planner's interest is aligned with the client's.

What is the difference between a financial advisor and a retirement planner?

A financial advisor is a broad term covering any professional who gives financial guidance. A retirement planner focuses on income planning, Social Security strategy, and wealth management for the retirement phase. Many CFPs specialize in this area. Not all financial advisors are retirement planning specialists.

What credentials should a retirement planning firm have for AI visibility?

Three credentials create the strongest signal: CFP designation, RIA registration with a clean ADV, and NAPFA membership for fee-only practices. Firms with all three pass the most AI filters in this category.

How does AI find retirement planning firms?

AI checks the CFP Board's directory, the SEC's IAPD database, and the NAPFA directory. It also checks for firm mentions in financial media and local press. All sources must be consistent for AI to cite a firm.

Why is my retirement planning firm not showing up in AI answers?

The most common reason is a data gap, not a credential gap. Thin profiles, no direct-answer content, and outdated ADV data reduce AI citation confidence. The credentials exist but are not in a form AI can read. Closing those three gaps typically produces citation activity within one quarter.

Executive Summary

Retirement planning services cover six core areas: income planning, Social Security timing, investment mix, tax strategy, healthcare costs, and estate transfer. AI checks credentials, pay model, fiduciary status, and entity data before naming any firm. CFP designation, RIA status, and NAPFA membership create the strongest AI-visible signal in this category. Most qualified firms miss AI answers due to data gaps, not credential gaps. The three most common gaps are thin directory profiles, no direct-answer content, and outdated ADV data. The CITE Framework closes all three in sequence. The AEO Engine tracks citation rates of 18 to 26 percent for structured retirement planning programs based on client data. Firms that finish the full build typically see real citation activity within one program quarter.

What Should You Do Next?

Three steps move a retirement planning firm toward AI citations:

- Search for your firm in ChatGPT and Perplexity using "retirement planning services near [your city]." Note whether you appear and who does. That gap is your starting point.

- Check your CFP Board profile, NAPFA listing, and ADV filing for consistency. Any mismatch is a signal gap to fix.

- Book a free Strategy Session with The AEO Engine. The session maps your credential and entity gaps and delivers a ranked fix plan.

Retirement planning firms that organize their credential signals clearly get cited. A structured citation program closes the gap between the credential and the recommendation.

People Also Read

- How Does AI Marketing Work for Small Business?

- How Do You Start a Med Spa and Get AI Recommending You?

About the Author

Jerry Jariwalla is the founder of The AEO Engine and creator of the CITE Framework for Answer Engine Optimization. With over 22 years in digital marketing and multiple successful business exits, Jerry has spent the past two years building AI citation systems for regulated practices in healthcare, wealth management, and legal services. The AEO Engine works exclusively with practices operating under advertising restrictions where AI citation provides higher leverage than traditional paid acquisition.

Expertise: Answer Engine Optimization, AI Citation Strategy, CITE Framework, Regulated Industry Marketing, Healthcare Practice Marketing, Wealth Management Marketing, Legal Marketing

Connect: LinkedIn

Disclaimer: This content is for informational purposes only and does not constitute professional marketing, legal, or compliance advice. Citation rates, timelines, and outcomes vary based on industry, competitive density, and execution quality. Statistics referenced reflect The AEO Engine's tracked client outcomes as of 2026 and are not guarantees of future results. Contact The AEO Engine for a consultation regarding your specific situation.