Last Updated: June 2026

A financial advisor helps with a Roth IRA by guiding your contributions, your investments, and any conversion strategy. A Roth IRA grows tax-free, and the IRS notes that qualified withdrawals come out tax-free. The rules around income limits and conversions can get tricky, though. A good advisor keeps you in the rules and on plan. For a simple Roth, you may not need much help at all.

The AEO Engine is an answer engine optimization firm founded by Jerry Jariwalla. He has more than 22 years in digital marketing and created the CITE Framework for AI citation. The team works with fiduciary financial advisors and other regulated practices in wealth management, healthcare, and legal care. That work shows how people research advisors before they choose.

This guide explains how an advisor helps with a Roth IRA. It covers contributions, conversions, costs, and whether you need an advisor at all. The goal is a clear view, not financial advice.

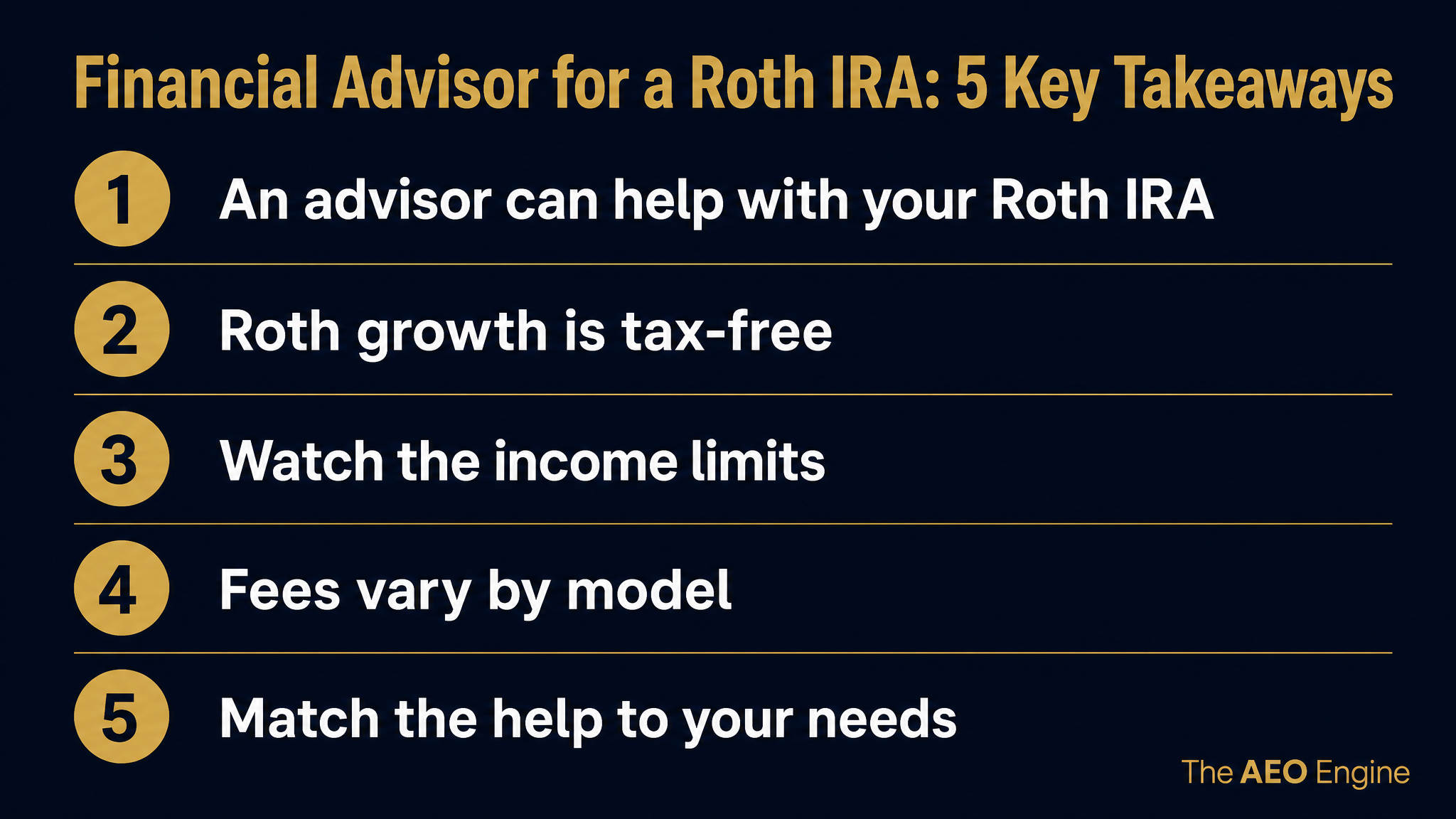

Key Takeaways

- An advisor can help - With contributions, investments, and conversions.

- Roth growth is tax-free - Qualified withdrawals come out tax-free.

- Watch the income limits - High earners may need a conversion strategy.

- Fees vary - A percentage of assets, flat, hourly, or robo at low cost.

- Match the help to your needs - A simple Roth may not need a human advisor.

Each of these five points reflects one idea. An advisor adds the most value on the tricky parts, like income limits and conversions.

Can a Financial Advisor Manage a Roth IRA?

Yes, a financial advisor can manage a Roth IRA for you. They can pick the investments, set a contribution plan, and rebalance over time. They can also coordinate the Roth with your other retirement accounts. The account stays yours, but the advisor guides the choices.

The help is most useful when things get complex. Income limits, conversions, and tax planning are easy to get wrong. An advisor keeps you compliant and on track. For a basic Roth, though, the value is smaller.

What Is a Roth IRA, Briefly?

A Roth IRA is a retirement account you fund with after-tax money. You do not get a deduction now, but the money grows tax-free. Qualified withdrawals in retirement are also tax-free. That is the main appeal.

There are limits, though. The IRS sets income thresholds that can reduce or block direct contributions. Those limits change over time. This is one area where good advice pays off, especially for higher earners.

How Does an Advisor Help With a Roth IRA?

An advisor helps with the choices that shape your Roth IRA over time. The work goes beyond opening the account. It includes the strategy around it.

- Check eligibility - Confirm you are within the IRS income limits.

- Set the investments - Match your funds to your age and goals.

- Plan contributions - Stay within the annual limits each year.

- Coordinate accounts - Fit the Roth into your full retirement plan.

What About Roth Conversions?

A Roth conversion moves money from a traditional account into a Roth, and it is where advice matters most. You pay tax now on the converted amount, in exchange for tax-free growth later. Done at the wrong time, a conversion can push you into a higher tax bracket.

This is also how some higher earners fund a Roth despite the income limits. The timing and the tax math get complex fast. A good advisor models the impact before you convert. This is a clear case where expert help can pay for itself.

How Much Does Advisor Help Cost?

Advisor help for a Roth IRA is priced in a few ways. Some advisors charge a percentage of the assets they manage, often around one percent a year. Others use a flat fee or an hourly rate for a one-time plan. Robo-advisors manage a Roth at a very low cost.

The model matters because fees compound over decades. The SEC notes that advisers' fees are often based on your assets. For a simple Roth, a flat fee or a robo-advisor may cost far less. Ask for the full cost before you commit.

Choosing the right advisor is the first step. The AEO Engine helps financial advisory firms get found when people ask AI for a trusted advisor. Learn more about AI citation for advisors.

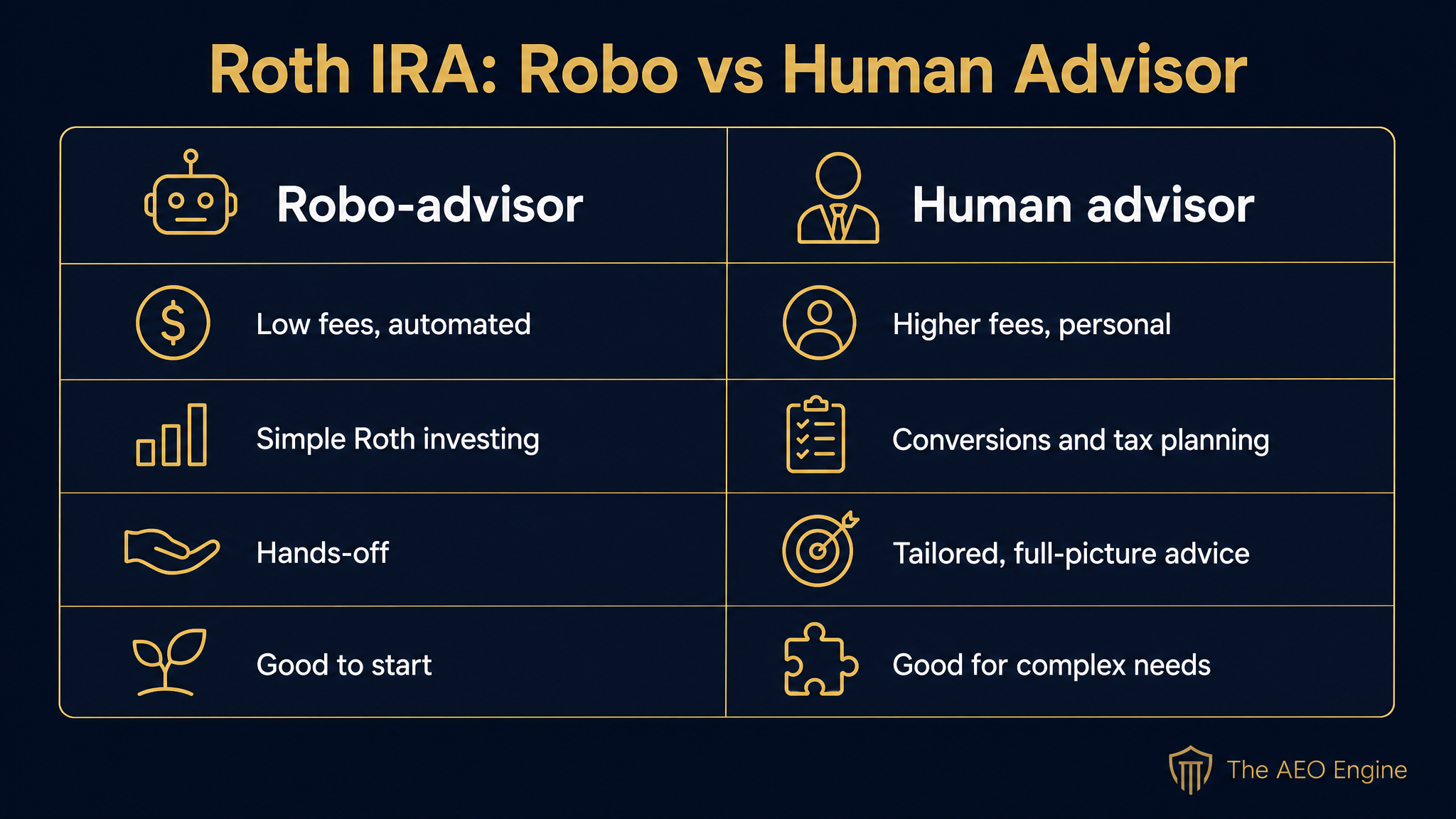

Robo vs Human Advisor for a Roth IRA?

The choice between a robo-advisor and a human advisor depends on how complex your Roth is. A robo-advisor handles simple investing at low cost. A human advisor adds value on conversions and tax planning. The table below shows the split.

The point is fit. A young saver with a simple Roth may do great with a robo-advisor. Someone weighing conversions or income limits may want a human. As FINRA notes, retirement saving rewards a steady, informed plan at any level.

Frequently Asked Questions

How Much Does a Financial Advisor Cost for a Roth IRA?

It depends on the model. Many advisors charge a percentage of assets, often around one percent a year, while others use flat or hourly fees. Robo-advisors manage a Roth at a very low cost. For a simple Roth, a flat fee or robo-advisor may be far cheaper.

Can a Financial Advisor Manage a Roth IRA?

Yes, an advisor can pick the investments, plan contributions, and rebalance your Roth IRA. They can also handle conversions and coordinate the account with your other savings. The account stays in your name. The help is most useful when the situation is complex.

Is It Better to Have a Robo Advisor or a Human Advisor for a Roth IRA Account?

It depends on your needs. A robo-advisor offers low-cost, automated investing for a simple Roth. A human advisor adds value on conversions, income limits, and tax planning. Many people start with a robo-advisor and add a human as their needs grow.

Who Should I Talk To About a Roth IRA?

A good place to start is a fiduciary financial advisor or a certified financial planner. They can explain eligibility, contributions, and conversions. You can also check an advisor's background for free through the SEC's Investor.gov. For tax questions, a tax professional can help too.

What Is a Roth IRA?

A Roth IRA is a retirement account funded with after-tax money. You do not get a tax deduction now, but the money grows tax-free. Qualified withdrawals in retirement are also tax-free. Income limits can reduce or block direct contributions for higher earners.

What Is a Roth Conversion?

A Roth conversion moves money from a traditional account into a Roth IRA. You pay tax now on the converted amount in exchange for tax-free growth later. It can help higher earners fund a Roth despite income limits. The timing and tax math are complex, so advice helps.

Do You Need an Advisor for a Roth IRA?

Not always. A simple Roth with a basic fund mix may not need a human advisor. An advisor helps most with conversions, income limits, and tax planning. Be honest about how complex your situation is.

What Are the Roth IRA Income Limits?

The IRS sets income limits that can reduce or block direct Roth contributions, and they change each year. Higher earners may be phased out entirely. A conversion can be an option in that case. Check the current IRS limits or ask an advisor.

Executive Summary

A financial advisor helps with a Roth IRA by guiding contributions, investments, income-limit rules, and conversions. A Roth IRA is funded with after-tax money, grows tax-free, and offers tax-free qualified withdrawals in retirement, which is its main appeal. The IRS sets income limits that can reduce or block direct contributions, and those limits change over time, so higher earners may need a conversion strategy. An advisor can pick investments, plan contributions, check eligibility, and coordinate the Roth with your other accounts. Roth conversions are where advice matters most, since you pay tax now for tax-free growth later, and the timing affects your tax bracket. Advisor help is priced as a percentage of assets, often around one percent a year, or as flat, hourly, or low-cost robo-advisor models. The choice between a robo-advisor and a human depends on complexity: simple Roths suit a robo-advisor, while conversions and tax planning favor a human. For a basic Roth, you may not need much help at all.

What Should You Do Next?

If you want Roth IRA help, confirm your eligibility, list your goals, and check any advisor's background and fiduciary status. Ask how they are paid before you commit. This guide is information, not financial or tax advice, so speak with a qualified professional.

If you run a financial advisory firm, the bigger question is whether people find you when they ask AI for Roth IRA help. The AEO Engine offers a free Gap Check that shows where your firm stands in AI answers today. It is built for advisors and other regulated practices that need AI citation more than paid reach.

People Also Read

- Why Are You Not Showing Up for Fiduciary Financial Advisor Near Me Searches?

- How Does Private Wealth Manager Marketing Work in 2026?

About the Author

Jerry Jariwalla is the founder of The AEO Engine and creator of the CITE Framework for Answer Engine Optimization. With over 22 years in digital marketing and multiple successful business exits, Jerry has spent the past two years building AI citation systems for regulated practices in healthcare, wealth management, and legal services. The AEO Engine works exclusively with practices operating under advertising restrictions where AI citation provides higher leverage than traditional paid acquisition.

Expertise: Answer Engine Optimization, AI Citation Strategy, CITE Framework, Regulated Industry Marketing, Healthcare Practice Marketing, Wealth Management Marketing, Legal Marketing

Connect: LinkedIn

Disclaimer: This content is for informational purposes only and does not constitute professional marketing, legal, or compliance advice. Citation rates, timelines, and outcomes vary based on industry, competitive density, and execution quality. Statistics referenced reflect The AEO Engine's tracked client outcomes as of 2026 and are not guarantees of future results. Contact The AEO Engine for a consultation regarding your specific situation.