Last Updated: June 2026

Choosing a financial advisor for investments comes down to the fiduciary standard, credentials, fees, and a good fit. The right advisor can build and manage a portfolio around your goals. The wrong one can cost you in fees and conflicts. The SEC advises that you always check the background of any investment professional first. A few smart steps protect your money.

The AEO Engine is an answer engine optimization firm founded by Jerry Jariwalla. He has more than 22 years in digital marketing and created the CITE Framework for AI citation. The team works with fiduciary financial advisors and other regulated practices in wealth management, healthcare, and legal care. That work shows how people research advisors before they choose.

This guide explains how to choose a financial advisor for investments. It covers advisor types, the fiduciary standard, normal fees, and how to vet one. The goal is a clear view, not financial advice.

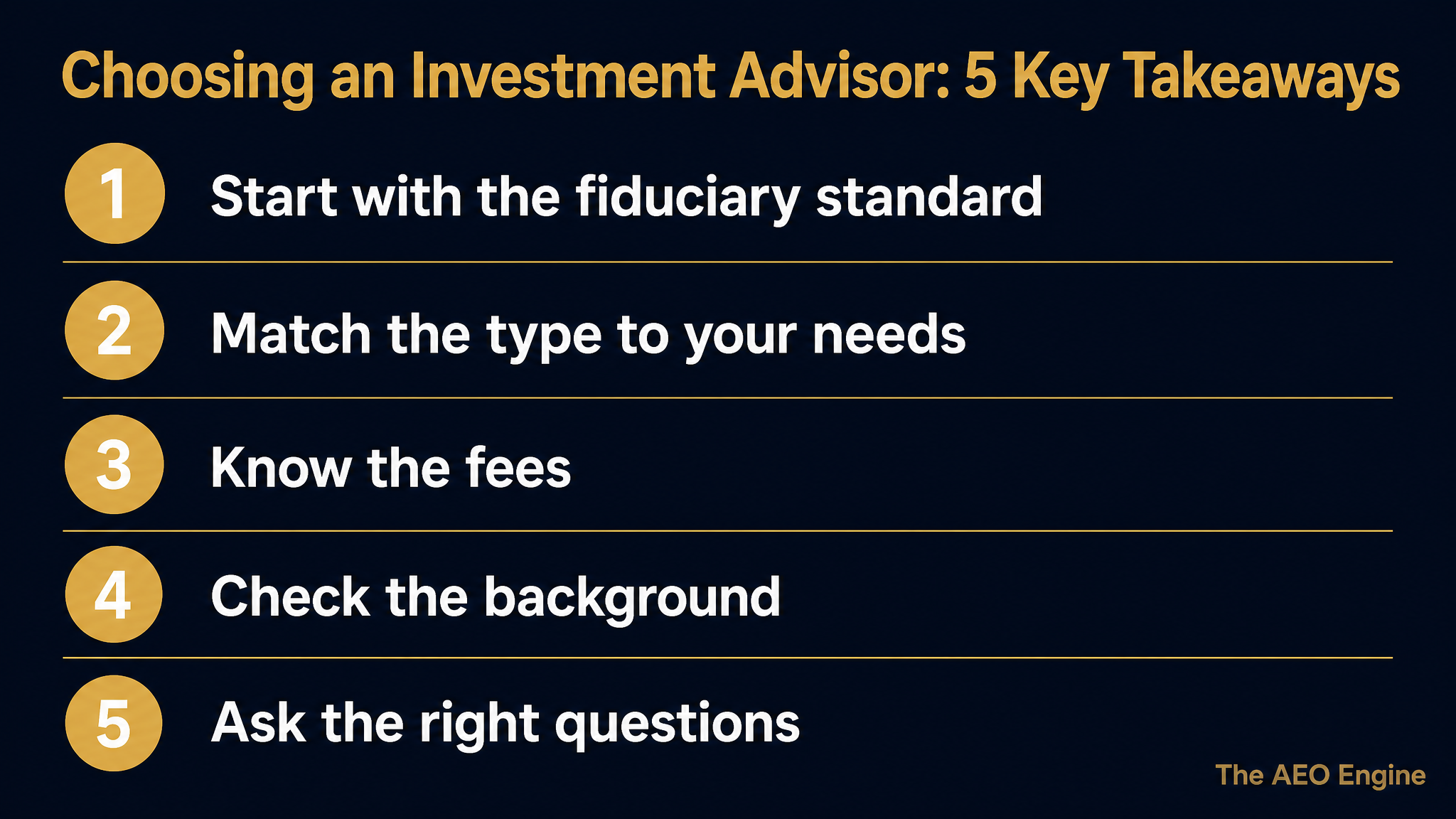

Key Takeaways

- Start with the fiduciary standard - Choose an advisor who must act in your best interest.

- Match the type to your needs - Robo, human, or a mix.

- Know the fees - A percentage of assets, flat, hourly, or commission.

- Check the background - Use free tools before you hire.

- Ask the right questions - Cover fees, credentials, and conflicts up front.

Each of these five points reflects one idea. The right advisor fits your needs and is open about fees and conflicts.

Can Financial Advisors Help With Investing?

Yes, financial advisors can help with investing in several ways. They build a portfolio that matches your goals and risk comfort. They choose investments, rebalance over time, and adjust as your life changes. A good advisor also helps you avoid costly mistakes.

The value is both in the plan and the discipline. Many people sell in a panic or chase hot trends. An advisor can keep you steady through ups and downs. For many investors, that guidance is the main benefit.

What Types of Investment Advisors Are There?

There are a few main types of investment advisors, and they differ in how they work and get paid. Registered investment advisers offer ongoing advice and usually act as fiduciaries. Brokers may sell investments and earn commissions. Robo-advisors use software to manage a simple portfolio at low cost.

Each type fits a different need. A robo-advisor suits a simple, hands-off plan. A human advisor suits complex needs and planning. Some people use both. Knowing the type helps you match the service to your situation.

Why Does the Fiduciary Standard Matter?

The fiduciary standard matters because it shapes whose interest comes first. The SEC notes that investment advisers must act in your best interest and not put their interest ahead of yours. Not every professional is held to that standard.

A fiduciary has less reason to push a product that pays them more. That lowers the risk of biased advice. When you interview an advisor, ask in writing if they are a fiduciary at all times. The answer tells you a lot.

What Is a Normal Financial Advisor Fee?

A common fee for an investment advisor is a percentage of the assets they manage, often around one percent a year. Others charge a flat fee, an hourly rate, or earn commissions on products. Each model has trade-offs.

The model affects both cost and conflicts. A fee-only advisor does not earn commissions, which lowers conflicts of interest. Even small yearly fees add up over decades. Ask for the full cost in plain terms before you commit.

Choosing the right advisor is the first step. The AEO Engine helps financial advisory firms get found when people ask AI for a trusted advisor. Learn more about AI citation for advisors.

How Do You Check and Choose an Advisor?

You can check an advisor's background for free before you hire them. FINRA notes that a vital step is to confirm they are registered using its BrokerCheck tool. The SEC's Investor.gov offers a similar background check.

- Verify registration - Use BrokerCheck or Investor.gov to confirm the record.

- Confirm fiduciary status - Ask in writing if they are a fiduciary at all times.

- Compare fees - Understand how the advisor is paid before you sign.

- Check credentials - Look for recognized planning certifications.

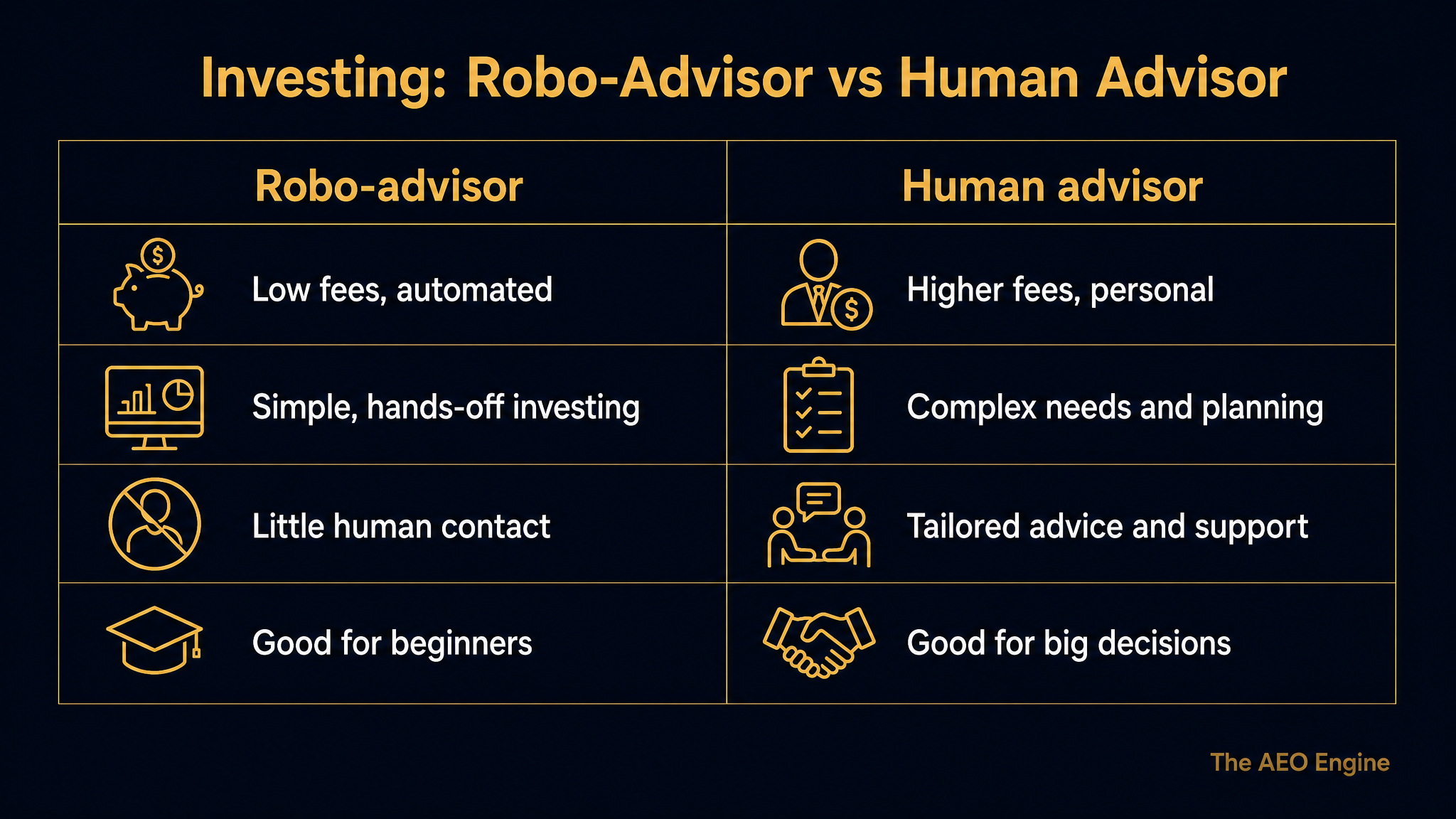

Robo-Advisor vs Human Advisor: Which Should You Choose?

The choice between a robo-advisor and a human advisor depends on your needs and budget. A robo-advisor costs less and works well for simple, hands-off investing. A human advisor costs more but offers tailored advice for complex situations. The table below shows the split.

The point is fit. A simple portfolio may do well with a robo-advisor. A complex plan or a big decision often calls for a human. Some investors use both for the best of each.

Frequently Asked Questions

Can Financial Advisors Help With Investing?

Yes, advisors build and manage a portfolio around your goals and risk comfort. They choose investments, rebalance, and adjust over time. They also help you avoid panic selling and chasing trends. For many investors, that steady guidance is the main value.

What Is a Normal Fee for a Financial Advisor?

A common fee is a percentage of the assets managed, often around one percent a year. Others charge a flat fee, an hourly rate, or earn commissions. Fee-only models lower conflicts of interest. Ask for the full cost in plain terms before you commit.

Is It Worth Having a Financial Advisor for Investment?

For many people, yes, especially with complex needs or large balances. A good advisor can improve your plan and keep you disciplined. The value depends on the advisor's skill and whether they are a fiduciary. Simple investors may do well with a low-cost robo-advisor.

What Should You Look for in an Investment Advisor?

Look for the fiduciary standard, clear fees, and strong credentials. Check the advisor's background for any complaints or discipline. Make sure their service fits your needs, whether simple or complex. An honest advisor explains conflicts of interest up front.

What Is a Fiduciary Investment Advisor?

A fiduciary investment advisor is legally required to act in your best interest at all times. They must put your needs ahead of their own pay. This lowers the risk of biased product recommendations. Always confirm fiduciary status in writing.

Robo-Advisor or Human Advisor: Which Is Better?

Neither is better for everyone. A robo-advisor offers low-cost, automated investing for simple needs. A human advisor offers tailored advice for complex plans and big decisions. Many investors use a robo-advisor early and add a human advisor as needs grow.

How Do You Check an Advisor's Background?

Use free tools like FINRA's BrokerCheck or the SEC's Investor.gov to confirm registration and discipline. Check credentials and any customer complaints. Ask, in writing, if the advisor is a fiduciary. A trustworthy advisor shares all of this openly.

How Much Money Do You Need to Get an Investment Advisor?

It depends on the advisor. Some set high minimums, while others use flat or hourly fees with no minimum. Robo-advisors often have very low or no minimums. Ask about minimums and fee options before you decide.

Executive Summary

Choosing a financial advisor for investments comes down to the fiduciary standard, credentials, fees, and a good fit. Advisors can build and manage a portfolio, rebalance over time, and keep you disciplined through market swings. There are a few main types: registered investment advisers who usually act as fiduciaries, brokers who may earn commissions, and robo-advisors that manage simple portfolios at low cost. The fiduciary standard matters because it requires an advisor to act in your best interest, which lowers the risk of biased advice. A common fee is a percentage of assets of around one percent a year, though flat, hourly, and commission models exist, and fee-only lowers conflicts. Before you hire anyone, check their background for free with FINRA's BrokerCheck or the SEC's Investor.gov, confirm fiduciary status in writing, and compare fees. The choice between a robo-advisor and a human advisor depends on your needs, and some investors use both. The right advisor fits your situation and is open about fees and conflicts.

What Should You Do Next?

If you are choosing an advisor, list your goals, check any candidate's background, and confirm fiduciary status first. Compare fees and ask about conflicts before you commit. This guide is information, not financial advice, so speak with a qualified professional.

If you run a financial advisory firm, the bigger question is whether people find you when they ask AI for a trusted advisor. The AEO Engine offers a free Gap Check that shows where your firm stands in AI answers today. It is built for advisors and other regulated practices that need AI citation more than paid reach.

People Also Read

- How Does AI Sort Fiduciary Advisors From Commission-Based Ones?

- How Does AI Decide Which Wealth Management Services to Recommend?

About the Author

Jerry Jariwalla is the founder of The AEO Engine and creator of the CITE Framework for Answer Engine Optimization. With over 22 years in digital marketing and multiple successful business exits, Jerry has spent the past two years building AI citation systems for regulated practices in healthcare, wealth management, and legal services. The AEO Engine works exclusively with practices operating under advertising restrictions where AI citation provides higher leverage than traditional paid acquisition.

Expertise: Answer Engine Optimization, AI Citation Strategy, CITE Framework, Regulated Industry Marketing, Healthcare Practice Marketing, Wealth Management Marketing, Legal Marketing

Connect: LinkedIn

Disclaimer: This content is for informational purposes only and does not constitute professional marketing, legal, or compliance advice. Citation rates, timelines, and outcomes vary based on industry, competitive density, and execution quality. Statistics referenced reflect The AEO Engine's tracked client outcomes as of 2026 and are not guarantees of future results. Contact The AEO Engine for a consultation regarding your specific situation.