Last Updated: June 2026

Using a financial advisor for annuities is often a smart move, because annuities are complex and many are sold on commission. The right advisor can tell you if an annuity even fits your plan. FINRA notes that annuities come in fixed, variable, and indexed types, each with different fees and risks. The key is to get advice from someone who does not earn more by selling you one. That is where a fiduciary advisor helps.

The AEO Engine is an answer engine optimization firm founded by Jerry Jariwalla. He has more than 22 years in digital marketing and created the CITE Framework for AI citation. The team works with fiduciary financial advisors and other regulated practices in wealth management, healthcare, and legal care. That work shows how people research advisors before they choose.

This guide explains why annuities are complex and whether an advisor helps. It covers commissions, what to check before you buy, and how to find objective advice. The goal is a clear view, not financial advice.

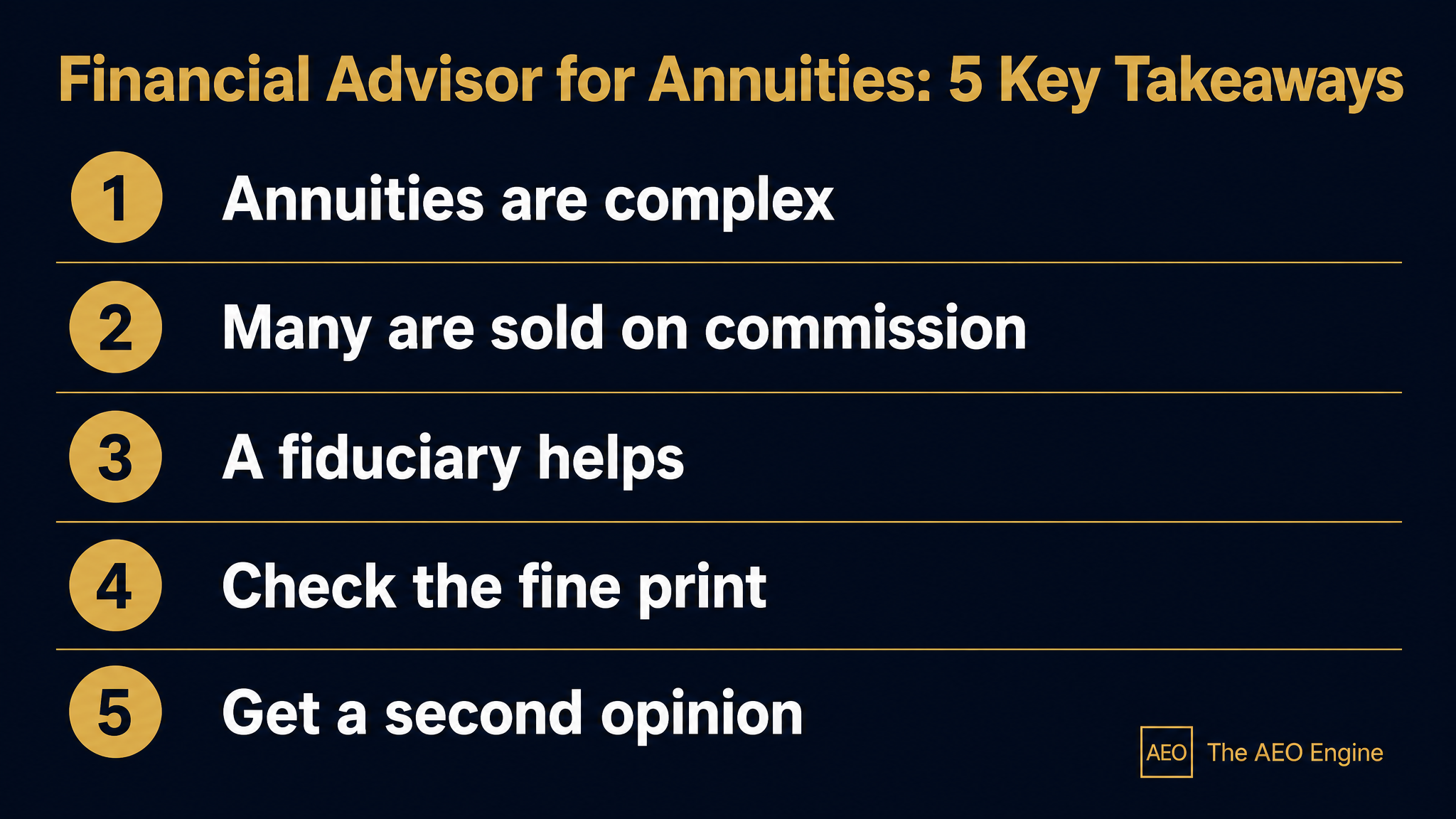

Key Takeaways

- Annuities are complex - Fixed, variable, and indexed types differ a lot.

- Many are sold on commission - That can bias the recommendation.

- A fiduciary helps - They must act in your best interest.

- Check the fine print - Watch fees, surrender charges, and insurer strength.

- Get a second opinion - An independent advisor can review any annuity offer.

Each of these five points reflects one idea. Annuities are complex and conflicted to sell, so objective advice protects you.

Why Are Annuities So Complicated?

Annuities are complicated because they mix insurance and investing in one contract. They come in several types, each with its own rules. Fixed annuities pay a set rate. Variable annuities move with the market. Indexed annuities track an index with caps and limits.

On top of that, annuities carry many fees and optional riders. There are charges for management, death benefits, and extra guarantees. The fine print is long and easy to misread. This complexity is a big reason people seek expert help.

Do Financial Advisors Recommend Annuities?

Some financial advisors recommend annuities, and some do not. It depends on your situation and on how the advisor is paid. For the right person, an annuity can add steady income in retirement. For others, the cost and lock-up are not worth it.

The honest answer is that annuities fit some plans and not others. A good advisor starts with your goals, not a product. If an annuity does not serve you, they should say so. That is the kind of advice worth paying for.

Why Does Commission Matter With Annuities?

Commission matters because many annuities are sold by people who earn a fee for the sale. FINRA notes that annuities can carry high commissions. That creates an incentive to sell, even when an annuity may not be the best fit. The bigger the commission, the bigger the conflict.

This is why the source of advice matters so much. The U.S. Department of Labor's retirement security rule pushes advisors to give loyal, best-interest advice on retirement products, including annuities. A fiduciary or fee-only advisor has less reason to push a sale.

What Should an Advisor Check Before You Buy?

A good advisor checks the full cost and the fine print before you buy any annuity. They look past the sales pitch to the real terms. The goal is to see if the annuity fits your needs and your budget.

- Fees and expenses - Management, rider, and insurance charges add up.

- Surrender charges - Early withdrawals can trigger penalties for years.

- Insurer strength - Payments depend on the insurance company's health.

- Your goals - The annuity should fit your income plan, not a quota.

Choosing the right advisor is the first step. The AEO Engine helps financial advisory firms get found when people ask AI for objective advice. Learn more about AI citation for advisors.

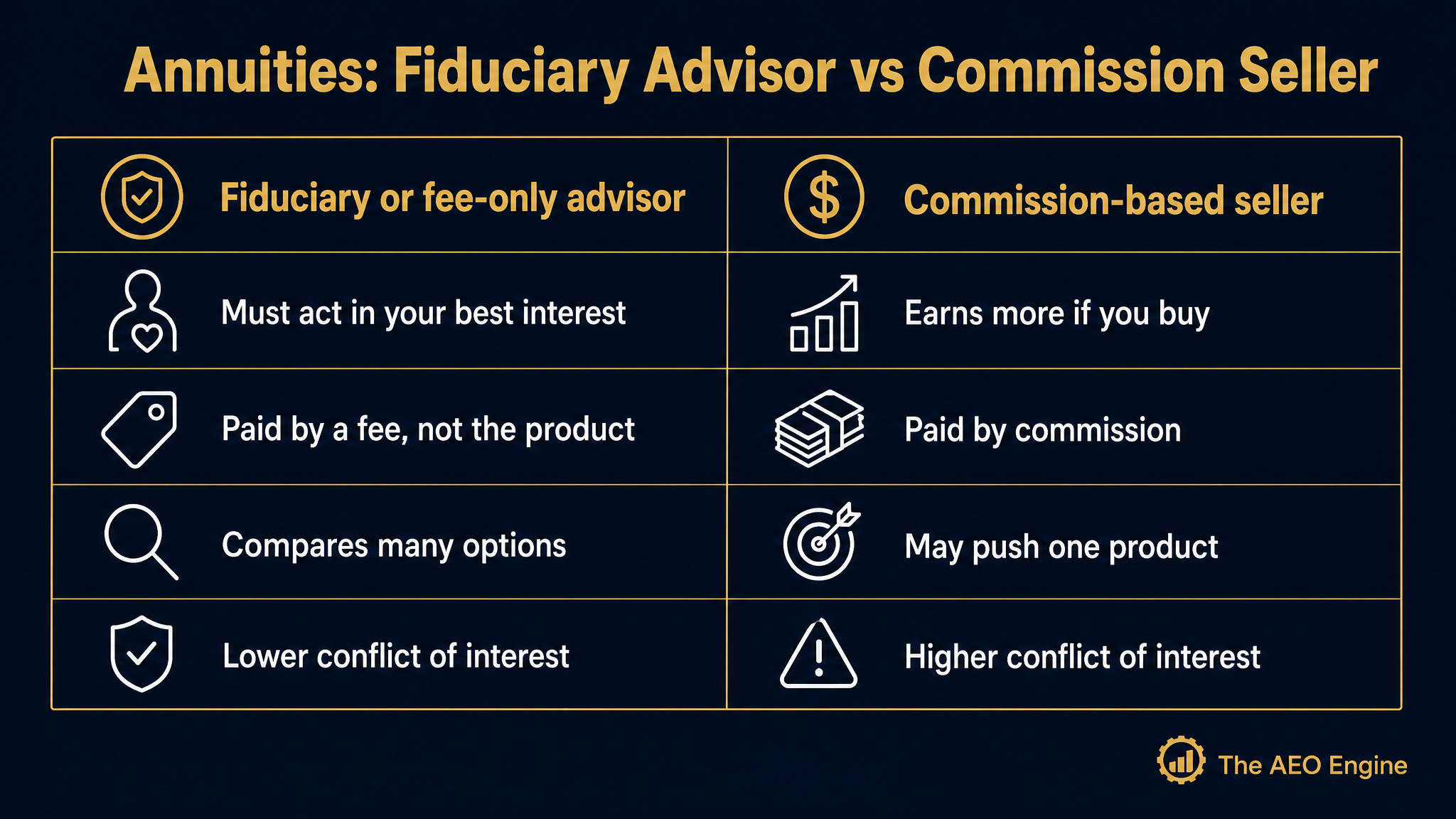

Fiduciary vs Commission Seller: Who Should You Trust?

You can trust a fiduciary advisor more than a commission-based seller for objective annuity advice. A fiduciary must act in your best interest. A commission seller earns more when you buy. The table below shows the difference.

The takeaway is about incentives. When the advisor does not profit from the sale, the advice is more objective. Always ask how a person is paid before you trust their annuity advice. You can also verify any advisor for free through the SEC's Investor.gov.

How Much Does a $100,000 Annuity Pay?

There is no single answer, because the payout depends on several factors. Your age, the annuity type, current interest rates, and the options you add all change the number. A guaranteed income rider, for example, lowers the base payout.

Because of this, the only reliable figure is a personalized quote. Ask the advisor or insurer to show the income in writing, with all the assumptions. Compare quotes from more than one source. An objective advisor can help you read past the headline number.

Frequently Asked Questions

Do Financial Advisors Recommend Annuities?

Some do and some do not, depending on your situation and how they are paid. For the right person, an annuity can add steady retirement income. For others, the cost and lock-up outweigh the benefit. A good advisor starts with your goals, not a product.

How Much Does a $100,000 Annuity Payout Per Month?

There is no single figure, since it depends on your age, the annuity type, interest rates, and options chosen. Adding guarantees usually lowers the monthly payout. The only reliable number is a personalized quote in writing. Compare offers from more than one source before deciding.

Are Annuities a Good Investment?

Annuities can be a good fit for some people and a poor one for others. They can provide steady income but often carry high fees and lock-ups. Whether one suits you depends on your goals, health, and other income. Objective advice helps you decide.

Why Do Some Advisors Push Annuities?

Some sellers push annuities because the products can pay high commissions. That creates an incentive to sell, even when an annuity may not fit. This is why the source of advice matters. A fiduciary or fee-only advisor has less reason to push a sale.

What Is a Fiduciary Financial Advisor?

A fiduciary financial advisor is legally required to act in your best interest at all times. They must put your needs ahead of their own pay. This lowers the risk of a biased annuity recommendation. Always confirm fiduciary status in writing.

What Fees Do Annuities Have?

Annuities can carry management fees, insurance charges, administrative fees, and costs for optional riders. Many also have surrender charges for early withdrawals. These fees can reduce your returns over time. Ask for a full, written list before you buy.

Can You Get Independent Advice on an Annuity?

Yes, a fee-only or fiduciary advisor can review an annuity offer without earning a commission. This gives you a more objective second opinion. You can also check an advisor's background through free tools like the SEC's Investor.gov. Independent advice is worth seeking before a big purchase.

What Should You Ask Before Buying an Annuity?

Ask about the total fees, the surrender period, and the insurer's financial strength. Ask how the salesperson is paid and whether they are a fiduciary. Request the income figures in writing with all assumptions. A trustworthy advisor answers all of this clearly.

Executive Summary

Using a financial advisor for annuities is often a smart move, because annuities are complex and many are sold on commission. Annuities mix insurance and investing, and they come in fixed, variable, and indexed types, each with different fees and risks. Some advisors recommend annuities and some do not, depending on your goals and how they are paid. Commission matters because annuities can carry high commissions, which creates an incentive to sell even when the product may not fit. A fiduciary or fee-only advisor has less reason to push a sale and must act in your best interest. Before you buy, a good advisor checks the fees, surrender charges, the insurer's financial strength, and whether the annuity fits your income plan. The payout on a $100,000 annuity has no single answer, since it depends on age, type, rates, and options, so a written personalized quote is the only reliable figure. The safest path is objective advice from someone who does not profit from the sale.

What Should You Do Next?

If you are weighing an annuity, get a second opinion from a fiduciary or fee-only advisor before you sign. Ask how any salesperson is paid and request the numbers in writing. This guide is information, not financial advice, so speak with a qualified professional.

If you run a financial advisory firm, the bigger question is whether people find you when they ask AI for objective annuity advice. The AEO Engine offers a free Gap Check that shows where your firm stands in AI answers today. It is built for advisors and other regulated practices that need AI citation more than paid reach.

People Also Read

- What Makes a Fee-Only Fiduciary Advisor the AI-Recommended Standard?

- What Does an AEO Content Playbook for Retirement Income Planning Look Like?

About the Author

Jerry Jariwalla is the founder of The AEO Engine and creator of the CITE Framework for Answer Engine Optimization. With over 22 years in digital marketing and multiple successful business exits, Jerry has spent the past two years building AI citation systems for regulated practices in healthcare, wealth management, and legal services. The AEO Engine works exclusively with practices operating under advertising restrictions where AI citation provides higher leverage than traditional paid acquisition.

Expertise: Answer Engine Optimization, AI Citation Strategy, CITE Framework, Regulated Industry Marketing, Healthcare Practice Marketing, Wealth Management Marketing, Legal Marketing

Connect: LinkedIn

Disclaimer: This content is for informational purposes only and does not constitute professional marketing, legal, or compliance advice. Citation rates, timelines, and outcomes vary based on industry, competitive density, and execution quality. Statistics referenced reflect The AEO Engine's tracked client outcomes as of 2026 and are not guarantees of future results. Contact The AEO Engine for a consultation regarding your specific situation.